This means when a company makes a sale on credit, it records a debit entry in the Accounts Receivable account, increasing its balance. Conversely, when the company receives a payment from a customer for a previously made credit sale, it records a credit entry in the Accounts Receivable account, decreasing its balance. Temporary accounts (or nominal accounts) include all of the revenue accounts, expense accounts, the owner’s drawing account, and the income summary account. Generally speaking, the balances in temporary accounts increase throughout the accounting year.

Normal Credit Balance:

This is important for accurate financial reporting and compliance with… The rest of the accounts to the right of the Beginning Equity amount, are either going to increase or decrease owner’s equity. With its intuitive interface and powerful functionality, Try using Brixx to stay on top of your finances and manage your growth.

What are Closing Entries in Accounting? Accounting Student Guide

- Ed’s inventory would have an ending debit balance of $40,000 and a debit balance in cash of $15,000.

- The double-entry system requires that the general ledger account balances have the total of the debit balances equal to the total of the credit balances.

- By having many revenue accounts and a huge number of expense accounts, a company will be able to report detailed information on revenues and expenses throughout the year.

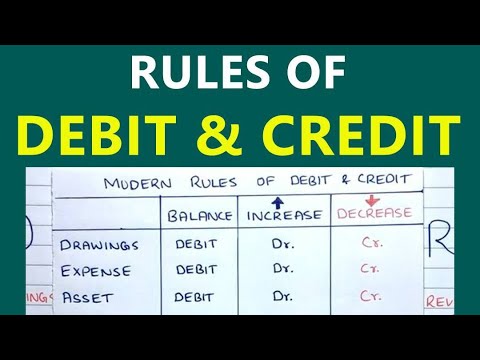

- The normal balance for each account type is noted in the following table.

- These are both asset accounts.He would debit inventory for $10,000 due to the new inventory and credit cash for $10,000 due to the cost.

Since cash was paid out, the asset account Cash is credited and another account needs to be debited. Because the rent payment will be used up in the current period (the month of June) it is considered to be an expense, and Rent Expense is debited. If the payment was made on June 1 for a future month (for example, July) the debit would go to the asset account Prepaid Rent. Here’s a simple table to illustrate how a double-entry accounting system might work with normal balances. A current asset account that reports the amount of future rent expense that was paid in advance of the rental period.

Normal balance FAQs

- Next, we’ll move on to adjusting these accounts with journal entries.

- Let’s recap which accounts have a Normal Debit Balance and which accounts have a Normal Credit Balance.

- This means that when you increase an asset account, you make a debit entry.

- Under the accrual basis of accounting, the Interest Revenues account reports the interest earned by a company during the time period indicated in the heading of the income statement.

- The rest of the accounts to the right of the Beginning Equity amount, are either going to increase or decrease owner’s equity.

If a company pays rent, it would debit the Rent Expense account. So, if a company takes out a loan, it would credit the Loan Payable account. Under the accrual basis of accounting the account Supplies Expense reports the amount of supplies that were used during the time interval indicated in the heading of the income statement. Supplies that are on hand (unused) at the balance sheet date are reported in the current asset account Supplies or Supplies on Hand. Revenues and gains are recorded in accounts such as Sales, Service Revenues, Interest Revenues (or Interest Income), and Gain on Sale of Assets. These accounts normally have credit balances that are increased with a credit entry.

AccountingTools

The gain is the difference between the proceeds from the sale and the carrying amount shown on the company’s books. Accounts Receivable is an asset account and is increased with a debit; Service Revenues is increased with a credit. Ed’s inventory would have an ending debit balance of $38,000. Accruing tax liabilities in accounting involves recognizing and recording taxes that a company owes but has not yet paid.

- He has $30,000 sitting in inventory and buys another 5 computers worth $10,000.

- Because of the impact on Equity (it decreases), we assign a Normal Debit Balance.

- Thousands of people have transformed the way they plan their business through our ground-breaking financial forecasting software.

- The contra accounts noted in the preceding table are usually set up as reserve accounts against declines in the usual balance in the accounts with which they are paired.

- This chart is useful as a quick reference to determine whether an increase or decrease in a particular type of account should be recorded as a debit or a credit.

- As noted earlier, expenses are almost always debited, so we debit Wages Expense, increasing its account balance.

- In accounting and bookkeeping, a debit balance is the ending amount found on the left side of a general ledger account or subsidiary ledger account.

What are the Normal Balances of each type of account?

It is the side of the account – debit or credit – where an increase in the account is recorded. Accounts Payable is a liability account, and thus its normal balance is a credit. When a company purchases goods or services on credit, which set of accounts below would have a normal debit balance? it records a credit entry in the Accounts Payable account, increasing its balance. Conversely, when the company makes a payment on its account payable, it records a debit entry in the Accounts Payable account, decreasing its balance.

- In accounting, a debit balance refers to a general ledger account balance that is on the left side of the account.

- It is possible for an account expected to have a normal balance as a debit to actually have a credit balance, and vice versa, but these situations should be in the minority.

- Salaries Expense will usually be an operating expense (as opposed to a nonoperating expense).

- Expenses normally have debit balances that are increased with a debit entry.

- Since expenses are usually increasing, think “debit” when expenses are incurred.